Finance Planning

Personal

Investing

Wealth Management

Risk Management

via Insurance Products

Retirement

Planning

Succession Planning

+ Estate Administration

Taxation

Tax Principles

Weekly Highlights

CBK Cuts Central Bank Rate from 10.75% to 10%

1. This week, treasury bills were oversubscribed, seeing the government

Financial Advice

Dividends: Why They Matter More Than You Think

When many people think of investing, they imagine buying and

Budgeting

Budgeting: A Guide for Small Business Owners

As a small business owners, you might constantly find yourself

Financial Advice

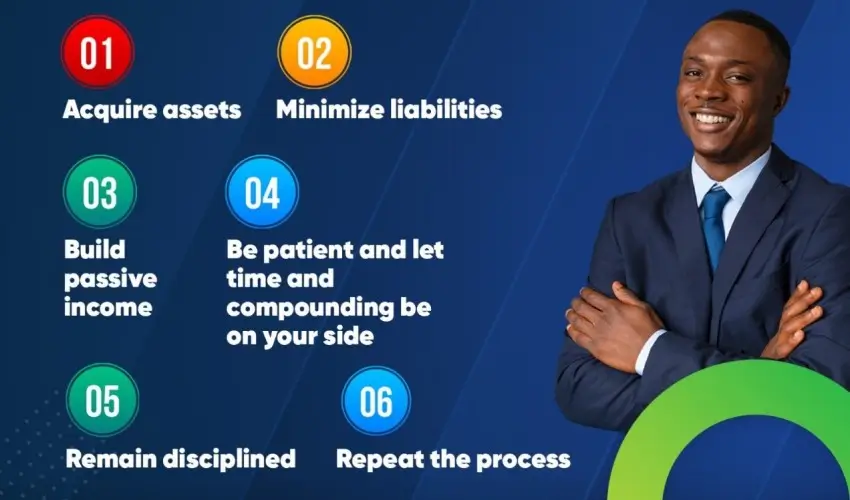

9 Money Habits that Lead to Success

You can adopt these practical habits for a financially sound

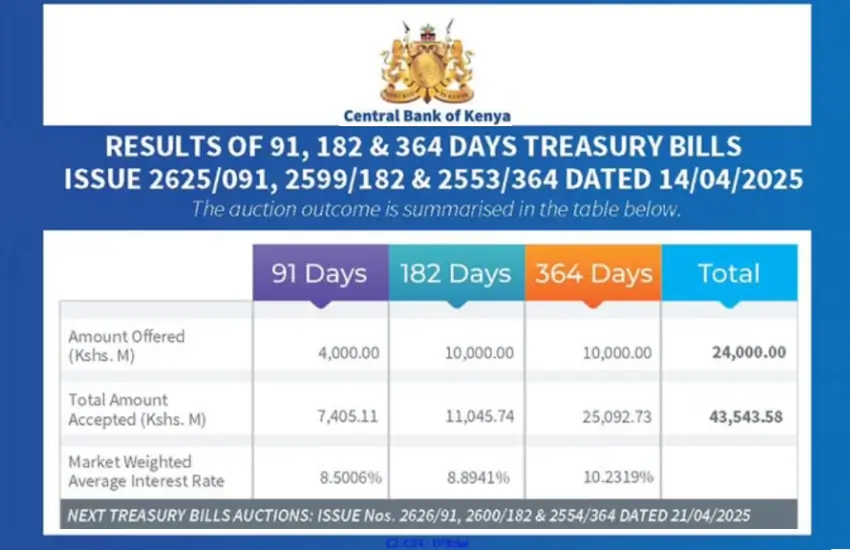

Weekly Highlights

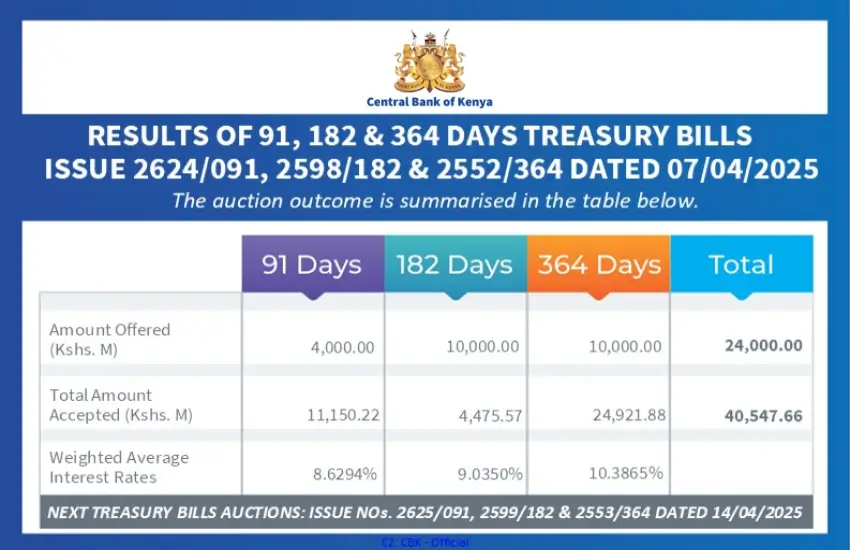

CBK Receives Ksh. 40.69 Billion Bids After Offering Ksh. 24 Billion Worth Of Treasury Bills

Here’s your round-up of this week’s key financial and corporate

Financial News

I&M Bank’s FY 2024 Results: A Year of Strong Growth and Promising Returns

I&M Bank has had an impressive year, with its FY

Weekly Highlights

KCB Group Records the Fastest Growth in Profitability, a 66.1% Increase to KES 60.09 Billion

It was a busy last week of the month as

Financial Advice

The Limitations of Relying on 1 Paycheck

Relying on a single paycheck is a risky lifestyle; a

"Abojani provides excellent training in financial literacy.

I attended their Personal Finance and Investing Masterclass that radically transformed my approach to handling money."

I attended their Personal Finance and Investing Masterclass that radically transformed my approach to handling money."

"The masterclass trainers are excellent and break down personal finance and basic financial accounting principles in such a simplified manner that anyone can understand. It brought a 360 degrees transformation to how I manage my finances"

"Abojani Investment community is a safe environment where financial literacy is strengthened and solidified, through provision of information on domestic and offshore fixed income and equity markets."

"If you are serious about gaining clarity of personal finance look no further. Abojani provides an excellent platform for this and more. Their Masterclass breaks down the financial matters in a simple and easy-to-grasp manner. Need I say more? Attend one!"

" Excellent!

If you re looking for Practical

Financial knowledge packaged in

easy to digest format...

ABOJANI is the place.

Best value for money !!! "

If you re looking for Practical

Financial knowledge packaged in

easy to digest format...

ABOJANI is the place.

Best value for money !!! "